Who Killed Affordable New York?

Struggling artists; vibrant locals; entitled college students. What could they all possibly have in common?

They are all scouring the internet for the best subletting deals on an influencer’s Instagram page.

New York City is home to nearly 8.5 million residents, and the dream city for billions more. With nearly 4 million housing-units available for citizens, we all cannot help but wonder: what do we do when units are technically in the regulated stock, but not available for us renters?

“Everyone acts like it’s normal,” one Brooklyn resident told me during an interview about apartment hunting in New York. “You stop asking whether the apartment is worth the price and start asking whether you can survive the rent.”

Is a City that Regulates, One That Can Also House?

Rent stabilization is a government tool that aims to regulate rent levels within a certain range. This differs from apartments that are “market-rate”, which have no legal control over what consumers can be charged. With Zohran Mamdani’s mayoral campaign focusing on attacking expensive rent levels from market-rate apartments, what is the value in a regulated apartment no one can find?

A study by the 2023 New York City Housing and Vacancy Survey found that the median monthly rent for a stabilized unit averaged around $1,500 while a market-rate unit averaged at around $2,000. This $500 gap represents relief for nearly 46% of stabilized tenants who are already paying more than 30% of their income on housing. For stabilized tenants earning below 50% of the Area Median Income (nearly 45% of renters in New York), that figure rises to 84%.

For hundreds of thousands of New Yorkers, this rent gap can be the difference between housing stability and displacement.

And yet, the citywide rental vacancy rate fell to a historic low of 1.41% in 2023. For stabilized units specifically, it was 0.98%. A city with a million regulated apartments and a near-zero vacancy rate is not a city where regulation is working as intended. Something is happening between policy and practice, and understanding that gap requires looking at what landlords do when regulation constrains their returns.

The Supply-Side Mechanism: When Regulation Discourages Availability

The most instructive case comes not from New York, but from San Francisco. In a landmark 2019 study, economists Diamond, McQuade, and Qian examined the effects of a 1994 rent control expansion and found that while covered tenants were nearly 20% more likely to remain in their homes, landlords responded by removing 15% of affected units from the rental market, primarily through condo conversions and redevelopment. The net effect was a 5.1% increase in citywide rents, as the shrinking supply of rentals pushed non-covered tenants into a tighter market.

The lesson is not that rent control fails its direct beneficiaries: it often does not. The lesson is that the costs are displaced onto precisely those renters who fall outside the system's protection.

New York's version of this dynamic took a sharper turn after the 2019 Housing Stability and Tenant Protection Act. Before HSTPA, landlords could raise rents significantly upon vacancy, creating a financial incentive to renovate and re-lease units. After HSTPA, vacancy decontrol was eliminated and Individual Apartment Improvement increases were capped, removing much of that incentive. According to the NYC Comptroller's office, the number of long-vacant stabilized units more than doubled from roughly 6,500 in 2017 to 13,400 in 2022. Ariel Property Advisors, drawing on NYC Department of Finance filings, estimates that nearly 20,000 units currently sit vacant because landlords cannot raise rents sufficiently upon vacancy to cover renovation costs.

The Comptroller's own 2024 report offers a more measured counterpoint, finding that distressed stabilized building values largely recovered to near pre-HSTPA levels by 2023, and that the number of truly distress-driven vacancies is likely smaller than industry groups claim. The truth appears to sit somewhere between those two accounts. A genuine vacancy problem exists. Its scale is contested.

Who Bears the Cost?

The distributional picture of rent stabilization is less straightforward than either its advocates or critics tend to acknowledge. Research by Zapatka and de Castro Galvao using NYC Housing Vacancy Survey data found that Hispanic and foreign-born households are significantly more likely to occupy stabilized units, while non-Hispanic Black households are actually less likely to live in stabilized apartments after controlling for unit and neighborhood characteristics. Access to the stabilized stock is not simply a function of income or need. It is stratified by race, national origin, and the accumulated advantage of having found a regulated unit and stayed in it.

This matters because it complicates the narrative that rent stabilization uniformly protects the most vulnerable New Yorkers. The system does provide meaningful rent relief to those inside it. But those outside it, often younger, more mobile, and less connected to the informal networks through which stabilized units are found and passed on, absorb the market-rate rents that are partly elevated because regulated units are unavailable. The Community Service Society documented that from 1968 to 2024, NYC rents rose 1,017% while all other consumer goods rose 826%. That divergence does not happen in a vacuum. It reflects, at least in part, the structural compression of available supply.

Employment in New York City grew 23% between 2010 and 2022, while the housing stock grew only 14%. This gap is a result of the regulatory frameworks being unable to match the rapid growth of the city. One of the largest attributes of the slow growth of housing stems from the cost of construction. A 2025 article by construction firm Turner & Townsend cited New York as one of the most expensive cities in the United States for construction markets because they harbor the highest labor costs. High demand for skilled labor only tightens that pressure, pushing costs further beyond what mid-market development can absorb. Additionally, an article by Manhattan Institute in 2021 argues that restrictive zoning locks out density across entire neighborhoods: single-family zoning alone restricts 17% of the residential area of Queens and 14% of Staten Island, making it legally impossible to build the mid-rise apartments that population growth demands.

Demand has structurally outpaced supply for over a decade, and rent stabilization, whatever its protective merits, does not build apartments. It redistributes access to existing ones.

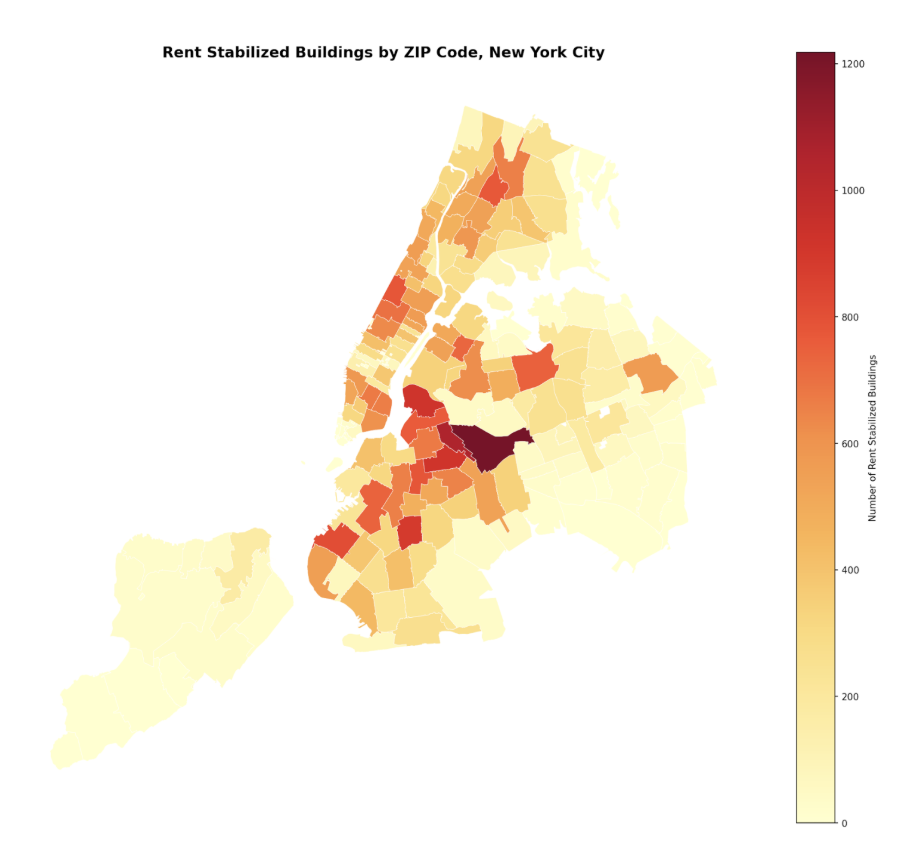

Figure 1: A heatmap showing the concentration of rent stabilized units within New York City

The Policy Tension: Reform Without Retreat

The standard economic critique of rent control is well established. According to the National Multifamily Housing Council’s report titled Rent Regulation Policy in the United States, they found that 93% of economists agreed rent ceilings reduce the quality and quantity of housing. They further reported that only 2% believed rent control had a positive net impact. These are striking numbers, though they measure professional consensus rather than objective certainty, and they predate the more nuanced recent literature that distinguishes between hard rent ceilings and softer stabilization regimes.

Perhaps the more productive question for New York is not whether they must regulate, but how to regulate in a way that does not generate the vacancy and supply dynamics described above. Zapatka and de Castro Galvao argue that expanded stabilization paired with new construction incentives could simultaneously curb rent inflation and limit displacement. The NYC Comptroller recommends targeted repair subsidies, code enforcement, and nonprofit acquisition of distressed stabilized buildings to bring long-vacant units back to market. These are not ideologically neutral proposals, but they engage seriously with the structural problem rather than treating it as a binary choice between regulation and a free market.

“Housing feels temporary now,” the resident reflected. “People come to New York already expecting they might eventually be pushed out.” That anxiety exists even among renters with stable employment, suggesting the issue extends beyond individual financial responsibility and toward broader structural instability within the city’s housing market.

What the data makes clear is that New York's housing crisis is not primarily a story of bad actors on either side. Instead, this is showing us a policy architecture that was designed for a different era, straining under the weight of population growth, cost inflation, and a legal reform that, while well-intentioned, reduced the financial incentive to keep regulated units in circulation.

Photo by Diane Picchiottino via Unsplash

Ananya is a sophomore at NYU from Pennsylvania, studying economics and business studies. She is passionate about current events related to startups and global economies. In her free time you can find her hunting Ticketmaster for cheap tickets!